Consider a routine continuous time optimization problem from economics:

V(t,a_{t}) :=

\max \int_{\tau=t}^{\tau = T}

e^{-\rho (\tau -t)} u(c_{\tau})d\tau

\text{ s.t. }

\dot{a}_{t} = y + ra_{t} - c_{t},

a_{0} \text{ given, } a_{T}=0.

Assume y & r are constants and u(c)=\frac{c^{1-\gamma}}{1-\gamma}.

The problem has a known closed form solution:

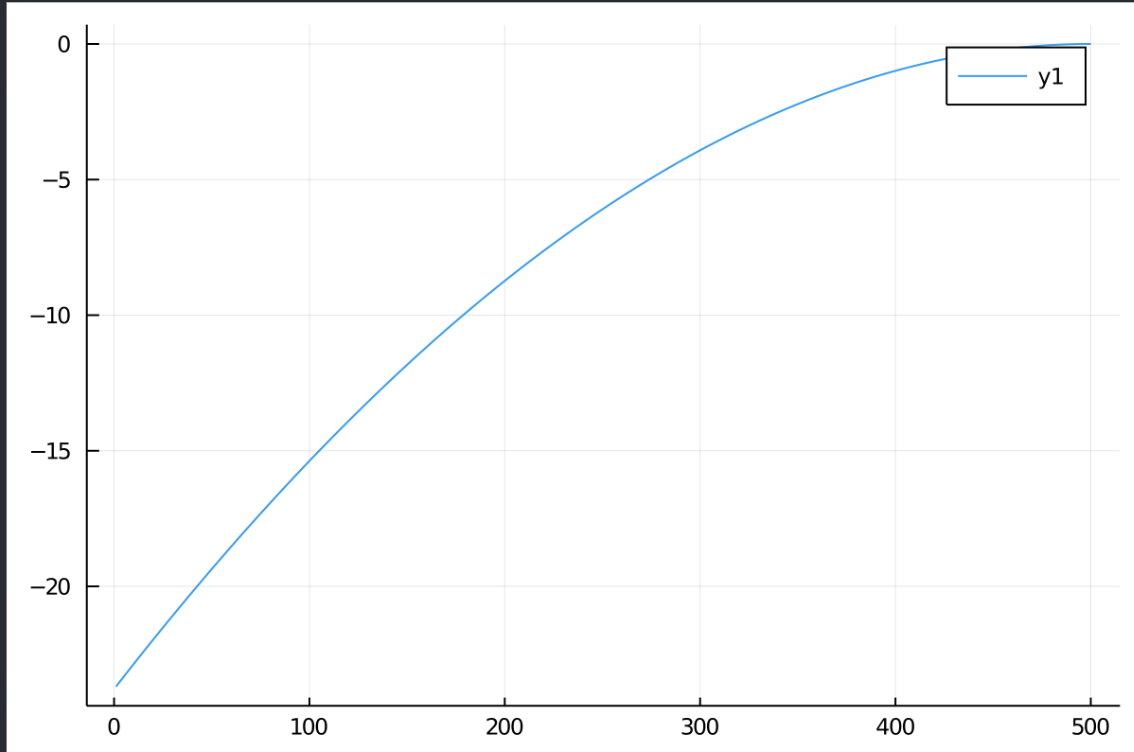

Here I plot V(0,a_{t}) and V(t,1):

To solve this using the HJB approach requires solving a PDE:

\left[\begin{array}{l}

\rho V(t,a_{t}) = \frac{c_{t}^{1-\gamma}}{1-\gamma} +

V_{a}(t,a_{t})\times \left(y + ra_{t} - c_{t} \right) + V_{t}(t,a_{t})

\\

c(t,a_{t}) = (V_{a}(t,a_{t}))^{-\frac{1}{\gamma}}

\\

V(T,a_{T}) = 0

\end{array} \right]

I’m trying to solve it w/ ModelingToolkit.jl, but it’s taking forever & not converging.

using NeuralPDE, Flux, ModelingToolkit, GalacticOptim, Optim, DiffEqFlux

using Plots

@parameters t a θ

@variables V(..)

@derivatives Da'~a

@derivatives Dt'~t

#

u(c,γ)= (c^(1.0 -γ))/(1.0 -γ);

γ = 2.00; ρ = 0.01; r = 0.01; y = 0.00; T = 5.0;

ω = r - (r-ρ)/γ;

# Closed form solution.

VS(t,a;y=y,r=r,γ=γ,ω=ω,T=T)=

u(a+(y/r), γ) * ( (1.0 - exp(-ω*(T-t))) / ω )^γ;

# if r=ρ

CS(t,a;y=y,r=r,γ=γ,ω=ω,T=T, a0=1) = (r*a0)/(1.0 - exp(-r*T) )

AS(t,a;y=y,r=r,γ=γ,ω=ω,T=T, a0=1) =

(a0)/(1.0 - exp(-r*T) ) +

a0*(1.0 - 1.0/(1.0 - exp(-r*T) ) ) * exp(r*t);

plot( VS.(0.0,0.01:.01:5.0) )

plot( VS.(0.0:.01:5.0,1.0) )

#

v = V(t,a,θ);

va = max(eps(), Da(V(t,a,θ)) );

vt = Dt(V(t,a,θ));

c = (va)^(-1.0/γ);

#uc = u(c,γ)

uc = (va^(1.0 - 1.0/γ) )/(1.0 - γ);

# HJB

eq = ρ*v ~ uc + va*(y + r*a - c) + vt;

# Boundary conditions

bcs = [V(T,a,θ) ~ 0.0] #0.f0

# Space and time domains

domains = [t ∈ IntervalDomain(0.0,5.0),

a ∈ IntervalDomain(0.0,5.0)]

# Discretization

dx = 0.1

# Neural network

dim = 2 # number of dimensions

chain = FastChain(FastDense(dim,16,Flux.σ),FastDense(16,16,Flux.σ),FastDense(16,1))

discretization = PhysicsInformedNN(dx,chain)

pde_system = PDESystem(eq,bcs,domains,[t,a],[V])

prob = discretize(pde_system,discretization)

cb = function (p,l)

println("Current loss is: $l")

return false

end

res = GalacticOptim.solve(prob, Flux.ADAM(); cb = cb, maxiters=10)

res = GalacticOptim.solve(prob, Optim.BFGS(); cb = cb, maxiters=10)

#

phi = discretization.phi

ts,as = [domain.domain.lower:dx/10:domain.domain.upper for domain in domains]

u_predict = reshape(

[first(phi([t,a],res.minimizer)) for t in ts for a in as],

(length(ts),length(as))

)

# plot V(t=0,a) #u_predict[1,:]

plot(as, u_predict[1,:])

# plot V(t, a=0.01)

plot(ts, u_predict[:,1])

- it takes forever & is not accurate

- originally I plugged in the exact equation but got an error

ERROR: DomainError with -0.05701087375174788:

Exponentiation yielding a complex result requires a complex argument.

Replace x^y with (x+0im)^y, Complex(x)^y, or similar.

- the issue is the pde has terms like V_{a}(t,a_{t})^{-\frac{1}{\gamma}} and we have numerical problems related to dividing by zero or taking the root of negative numbers.

We would like to use the prior knowledge that V_{a}>0. - following a suggestion @matthieu , I tried

max(eps(), va)^(-1/γ)

No more domain error, but it takes forever & is not accurate.

Note: if \gamma >1 the trivial solution V(t,a_{t})=0 also satisfies the PDE.

It can be avoided w/ a bequest motive…