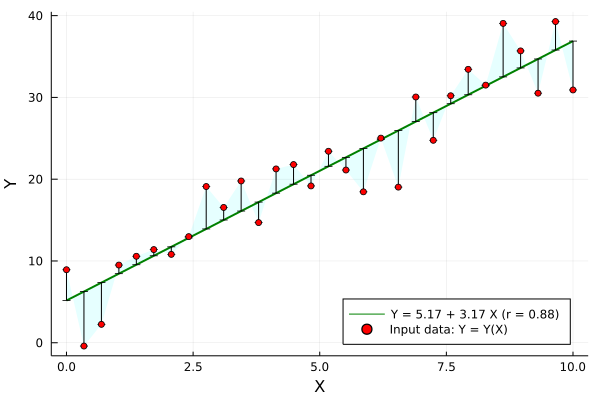

Just in case it might be useful, sharing one linear regression example below, where the correlation coefficient r is displayed and other regression statistics are computed too:

using Plots, Random, Distributions, GLM, DataFrames, Printf

# input data

n = 30

x = LinRange(0,1, n) .* 10

e = rand(Normal(0,mean(x)/4),n)

parms = Dict(:b0 => 6, :b1 => 3.2)

y = parms[:b0] .+ parms[:b1] .* x .+ 3*e

data = DataFrame(X=x, Y=y)

# linear regression

ols = lm(@formula(Y ~ 1 + X), data)

a, b = coef(ols)

r = r2(ols)

# plotting

yhat = parms[:b0] .+ parms[:b1] .* x

err = y - yhat; z0 = 0*err;

str = "Y = " * @sprintf("%.2f",a) * " + " * @sprintf("%.2f",b) * " X (r = " * @sprintf("%.2f",r) * ")"

plot(x,yhat, label=str, lw=2, c=:green, yerror=(z0,err), ribbon=(z0,err), fc=:cyan, fa=0.1)

scatter!(x, y, mc=:red, xlabel="X", ylabel="Y", label="Input data: Y = Y(X)", legend=:bottomright)

Some stats output after command:

julia> ols = lm(@formula(Y ~ 1 + X), data)

Y ~ 1 + X

Coefficients:

───────────────────────────────────────────────────────────────────────

Coef. Std. Error t Pr(>|t|) Lower 95% Upper 95%

───────────────────────────────────────────────────────────────────────

(Intercept) 5.16706 1.31032 3.94 0.0005 2.48298 7.85113

X 3.172 0.225023 14.10 <1e-13 2.71106 3.63294